Harvey and Irma

What are the likely ongoing effects from Harvey and Irma on the propane industry?

Much has been written about propane supply and demand changes since Harvey and Irma. There are a lot of things happening at once, pushing and pulling prices, and much of what’s happening is still changing daily.

The consequences of every supply addition or demand subtraction from the pre-hurricanes equation is felt both here and abroad.

Should we be worried?

There’s a lot of hype right now over our “perceived low” propane inventory situation. I think it’s a little overdone.

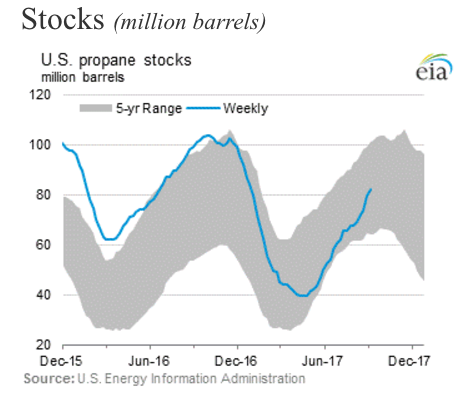

- Propane inventories currently stand at 80.80 mmbbls. They typically build well into October, so we still should end up near or above 90 mmbbls. which would be our third highest level ever heading into winter.

- Propane is trading near 75% of crude. I don’t think that’s sustainable. Only two years in the past 30 years has propane traded at 80% or higher. (You’ll have to go back 17 years to find the last time.)

- Much has also been made of this year’s corn crop. It’s still early since only 30% of the corn in Iowa has reached maturity (the largest corn-producing state), but so far, only 59% of the corn is rated good to excellent. Crops mature rapidly with above-average temps and below-average moisture. With much of Iowa in extreme drought status (half of all farmers report "short to very short" topsoil moisture) and a projected forecast of near-record warm temperatures, prospects for a late, wet crop (high propane demand) are diminishing.

What about Harvey?

Curtailed propane exports, along with diminished petrochemical demand (both from infrastructure damage, as well as a significant ethane feedstock price advantage), outweighed the Gulf Coast propane production loss for the past few weeks.

Consequently, we saw a two-week period with an above-average inventory build, even though the conditions that contributed to the magnitude of the anomaly (8.63 mmbbls.) were temporary. We’ve since seen a 1.4 mmbbl. draw for the week ending 9/15/17 which reflects a 4.0 million barrel increase in export demand. This is due, of course, to the Houston ship channel reopening, and the large increase in export activity may also be an anomaly, since the weekly export number is nearly double the reported numbers shortly before Harvey. But we’ll need to keep a close eye on export levels, since they dominate all other forms of propane demand in our industry.

Consequently, we saw a two-week period with an above-average inventory build, even though the conditions that contributed to the magnitude of the anomaly (8.63 mmbbls.) were temporary. We’ve since seen a 1.4 mmbbl. draw for the week ending 9/15/17 which reflects a 4.0 million barrel increase in export demand. This is due, of course, to the Houston ship channel reopening, and the large increase in export activity may also be an anomaly, since the weekly export number is nearly double the reported numbers shortly before Harvey. But we’ll need to keep a close eye on export levels, since they dominate all other forms of propane demand in our industry.

When trying to make sense of the recent roller-coaster weekly inventory numbers, it’s important to step back and look at the three-week average (post-Harvey) which shows a 2.4 mmbbl. average weekly build. That’s still an above-average build level for this time of year.

What about Irma?

Irma caused heart-breaking and destructive damage to Florida, but no appreciable impact on the production or supply of propane. The short-term impact should be on the demand side, not supply, since the devastation from both hurricanes should negatively affect US gross domestic production for a while. In simple terms, GDP is a measure of everything we make, buy, or sell.

In the mid-term, we expect that demand for energy to rebuild areas damaged by both hurricanes will pick up substantially.

How are your customers handling higher prices?

Understandably, your customers never appreciate higher propane prices, but folks know that Harvey affected the Houston area energy business, and they are more accepting of higher prices as long as the price at the gasoline pump keeps going up. That’s their price barometer!

EIA Numbers for the Week:

Propane inventories showed a draw of 1.4 mmbbls. and currently stand at 80.8 mmbbls. (20% behind last year), but they are now in the middle of the five-year average range.

What’s Happening with Propane Prices?

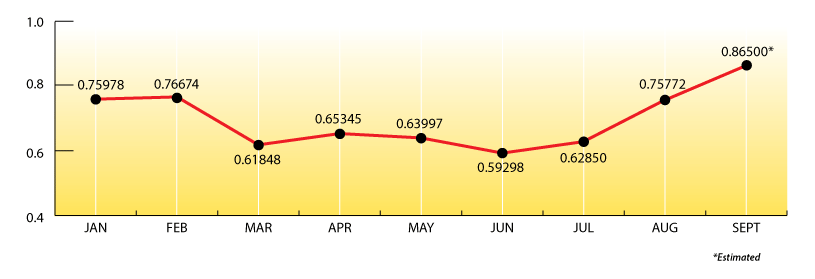

Here are the Mt. Belvieu monthly averages for the past nine months with a projection for September:

The Skinny:

Back in May and June, we mentioned that prices were at a fair level and that upside risk was greater than downside opportunity. Our recommendation was that customers convert a portion of their index-priced supply contracts over to a fixed price. Fortunately, many folks followed our recommendation. There is still time to cover your fixed-price commitments with your customers. Just give us a call!

Many folks are nervous about this coming winter, mostly in terms of propane supply and the distribution chain. But please be assured that we are well-prepared to meet your upcoming propane requirements. We have assembled one of the most diversified, expanding portfolios of supply distribution points in the Northeast, and with many decades of midstream propane experience, we’re ready to help guide you through the challenges ahead.

Get Stephen's insights on propane delivered to your inbox every month.

Sign up for our email newsletter here.

NOTE: The views and opinions expressed herein are solely those of the author, unless attributed to a third-party source, and do not necessarily reflect the views of Ray Energy Corp, its affiliates, or its employees. The information set forth herein has been obtained or derived from sources believed by the author to be reliable. However, the author does not make any representation or warranty, express or implied, as to the information’s accuracy or completeness, nor does the author recommend that the attached information serve as the basis of any buying decision and it has been provided to you solely for informational purposes.

© 2011-2017 Ray Energy Corp. All rights reserved. Any reproduction, representation, adaptation, translation, and/or transformation, in whole or in part by whatsoever process, of this site or of one or several of its components, is forbidden without the express written authorization from Ray Energy Corp.