The Not-So-Ancient Mariner

What could the Mariner 2 pipeline delay and the backwardation in propane prices mean for us in terms of supply and pricing this winter?

What could the Mariner 2 pipeline delay and the backwardation in propane prices mean for us in terms of supply and pricing this winter?

“We cannot direct the wind, but we can adjust the sales.” − Calloway

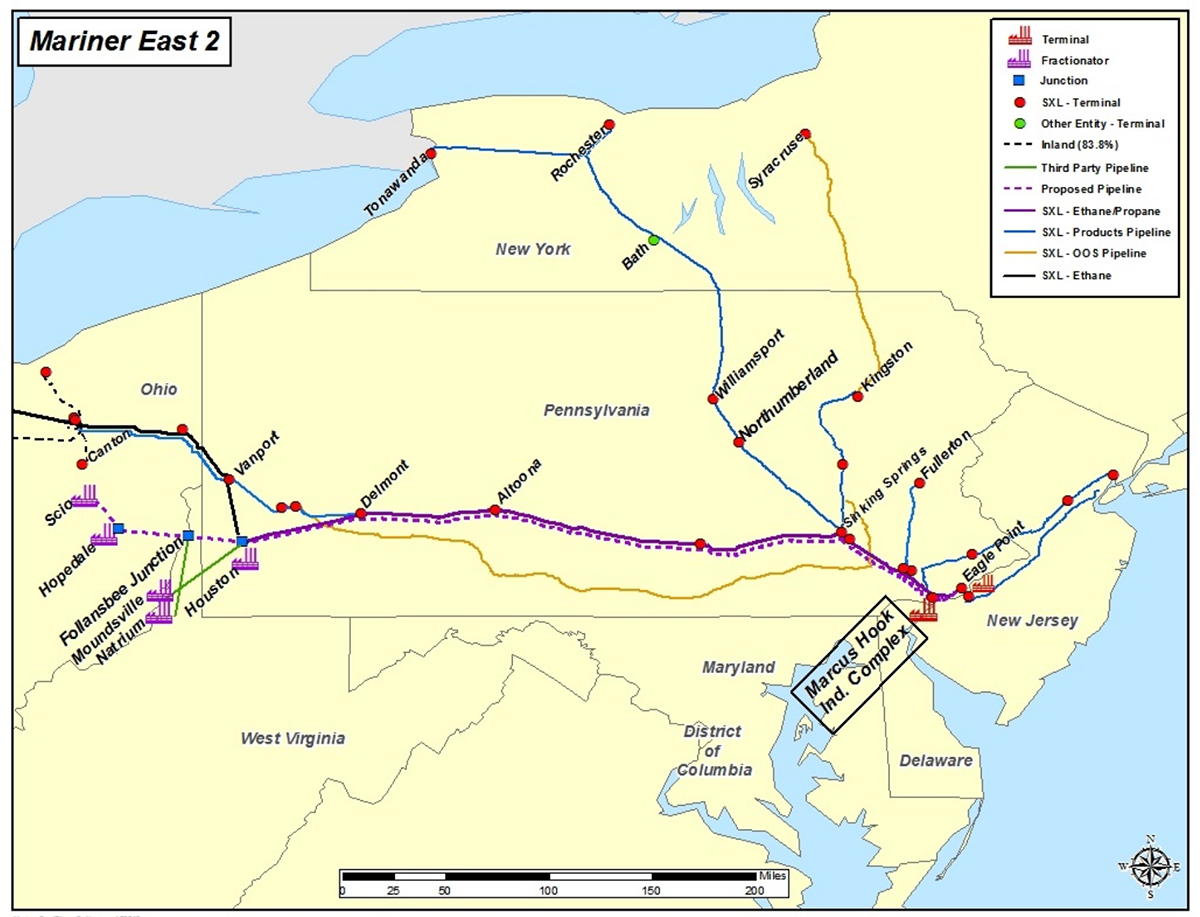

Mariner East 2

By now, you’ve probably heard about Mariner East 2 (ME2). Since the pipeline is in our backyard, it’s one of those things we feel that we should understand, even if we’re a little confused. So let's walk this through.

To begin, it was just announced that the operation of the pipeline has been delayed until next spring, from an original start date of November. This isn’t a surprise to anyone … least of all anyone involved in shipping natural gas liquids (NGLs) to Marcus Hook, PA, for the export market.

The capacity of this second Mariner pipeline is approximately 11.5 million gallons per day of propane, butane, and ethane.

The capacity of this second Mariner pipeline is approximately 11.5 million gallons per day of propane, butane, and ethane.

Much of the propane supply that was scheduled to be shipped on ME2 and then exported from the East Coast now needs to find a way onto ships along the Gulf Coast. To do that, 100 +/- railcars at a time (called unit trains) are sent from the Marcellus and Utica shale regions of WV, OH, and western PA to Conway, KS. The supply is then piped to the Gulf Coast for waterborne exports.

What does that mean for us?

Not all of this new propane supply earmarked for Marcus Hook, PA, is going to the Far East via Kansas. Much of it is still going to Marcus Hook, but by rail instead of pipeline.

If that propane supply is truly needed here in the Northeast this winter (meaning we’ll pay more than the international market), it will stay here.

How can backwardation in the propane market affect prices?

This summer our propane market switched from a market that was in contango (worth more each month), which encourages storing production, to a market in backwardation (worth less each month) which discourages storing production.

Backwardation occurs because supply tightness exists, but the conditions that created the tightness in the current month are not expected to be present in the future months. The monthly price difference can be minimal or it can be great.

The backwardation for propane between the first quarter of 2018 and the second quarter of 2018 has recently been near a record discount of 17 cents per gallon. And the recent Brent crude discount of $2/bbl. one year out is the largest in three years!

A commodity market in backwardation is fundamentally bullish. Why? The consumer is telling the producer, “We can’t wait − we need it now.”

How can that lead to price spikes?

The folks that make our propane are selling as much as they can. There is no incentive for them to pay to go into and out of storage, only to sell a few months from now at a discount. It is far better to collect a premium now.

The “sell now” mentality is in overdrive. Unfortunately for us, the international customer is the preferred customer. If we want to move up to first class, we’ll need to pay for the upgrade.

In our October 2016 blog, we wrote:

- “What is the world willing to pay?”

- “The concern will be when the world community tries to outbid the US for our [abundant] propane supply, regardless of price.”

In the last six months, we’ve seen little retail demand and low petrochemical demand for propane. If retail and petrochemical demand pick up, an international bidding war is possible for the propane we make and the propane we have in storage. Monthly demand could begin to greatly exceed monthly supply since the folks that make our propane are already selling all they can.

Do you have any good news?

I do, bear with me.

Crude prices dropped under $50/bbl. in May and rig counts have been on a declining trend since this summer. So, when WTI crude oil prices moved back over $50/bbl.in September, I thought we’d see increases in rig counts (an indicator of future production) within eight weeks (the average lag time). But we haven’t, until recently.

Baker Hughes publishes oil and gas rig counts. This past week they reported that the US added nine oil rigs, the greatest weekly increase since June, bringing the total to 738 (versus 452 last year). With oil prices now at two-year highs, this rig count trend should continue and help propane production.

Charlie Brown football.

Our energy industry is mercurial. Crude oil prices and rig counts are up, down, up. It reminds me of the Charlie Brown cartoon where Lucy keeps pulling the football away from Charlie, each time reassuring him she won’t do it again! In this case, the “football” is $50/bbl. crude oil.

ConocoPhillips is one of the largest oil and gas producers in the country and they plan to spend $5.5 billion per year as long as oil prices stay above $50/bbl. It sounds encouraging. But what if Lucy pulls the ball away again?

Are there other reasons why we aren’t producing more crude oil and natural gas now?

Backwardation may also explain the lack of enthusiasm from US exploration and production. For two years now it’s been tough to finance exploration projects when the future market discounts haven’t allowed companies to lock in acceptable returns. And that has been the strategy behind OPEC’s short-term production cuts all along.

What can turn this ship around?

Since nearly 50% of all US propane production is exported now (about 42 million gallons per day or the equivalent of three very large ships per day), the only thing that can help propane levels is expanding production and declining export demand.

- Expanding production: higher crude oil prices and rig counts, along with stable natural gas prices, may mean we’re turning the corner.

- Declining export demand: high prices should create demand destruction. “Sorry, but at these prices I think I’ll go back to burning cow dung!”

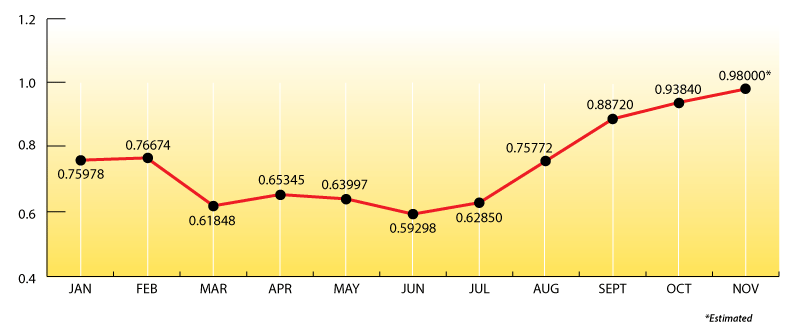

What’s happening with propane prices?

My best guess for a short-term price range for Mt. Belvieu, TX, propane is $0.79 to $1.20. A break above $1.20 could lead the way to $1.60.

Here are the Mt. Belvieu monthly averages for the past 11 months with a projection for November:

EIA numbers for the week:

Propane inventories drew down a larger than expected 2.52 mmbbls. to 74.68 mmbbls. for the week ending 11/10/17. Total U.S. inventories are 26% behind last year.

The Skinny:

Our Northeast propane industry doesn’t really have a supply problem. We have a complacency problem. And that’s understandable. After all, we’ve had two mild winters in a row. But now, we’ve set ourselves up to compete against the rest of the world this winter for approximately 75 to 100 million incremental gallons (10% to 15% projected under-contract amount).

Blessing:

Thanksgiving dinner at my grandmother’s house in Connecticut always started with “Gunny” saying the blessing: “Bless us, O Lord, for these thy gifts which we are about to receive, from thy bounty.”

All of us at Ray Energy are truly thankful for our wonderful bounty of family and friends, many of whom are reading this now. And we hope you take comfort in knowing that we’re well prepared to meet your upcoming propane requirements.

Get Stephen's insights on propane delivered to your inbox every month.

Sign up for our email newsletter here.

NOTE: The views and opinions expressed herein are solely those of the author, unless attributed to a third-party source, and do not necessarily reflect the views of Ray Energy Corp, its affiliates, or its employees. The information set forth herein has been obtained or derived from sources believed by the author to be reliable. However, the author does not make any representation or warranty, express or implied, as to the information’s accuracy or completeness, nor does the author recommend that the attached information serve as the basis of any buying decision and it has been provided to you solely for informational purposes.

© 2011-2017 Ray Energy Corp. All rights reserved. Any reproduction, representation, adaptation, translation, and/or transformation, in whole or in part by whatsoever process, of this site or of one or several of its components, is forbidden without the express written authorization from Ray Energy Corp.