Limbo Dancing Propane Prices

How Limber Are Propane Prices?

Limbo dancing originated in Trinidad and Tobago. It was traditionally performed at wakes to symbolize the transition from one life to another.

With propane prices about 30 percent lower than the March peak, folks are wondering, “How low can prices go?”

And, how do we make sense of the fact that energy prices are falling, yet physical markets remain fairly tight?

The Energy Crisis, One Month Later.

Just last month, International Energy Agency (IEA) Director Fatih Birol said: “The world has never witnessed such a major energy crisis in terms of its depth and complexity.”

Echoing that sentiment, here are two quotes from a front-page New York Times article, just 18 days ago, titled: "E.U. Scrambling for Gas Options to Avert a Crisis".

“There is a very big and legitimate worry about this winter.”

– Michael Stoppard, VP Global Gas Strategy, S & P Global, a research firm.

“We are getting close to the danger zone.”

– Massimo Di Odoardo, VP Gas, Wood Mackenzie, a research institution.

Fast forward to today when OPEC Secretary General Haitham Al Ghais cautioned, "we are running on thin ice," regarding strong global demand and less spare capacity.

So what's going on? Have the fundamentals changed that much? Or is this the calm before the storm?

More Demand For Natural Gas.

Most of us know that natural gas is the primary source of propane. It’s also the main source of electric power generation in America.

Strong demand for electricity = strong demand for natural gas.

Henry Hub prices have been fairly quiet for about 14 years now after hitting high notes above $17.00 per mmBtu back in 2000, 2003, 2005, and 2008.

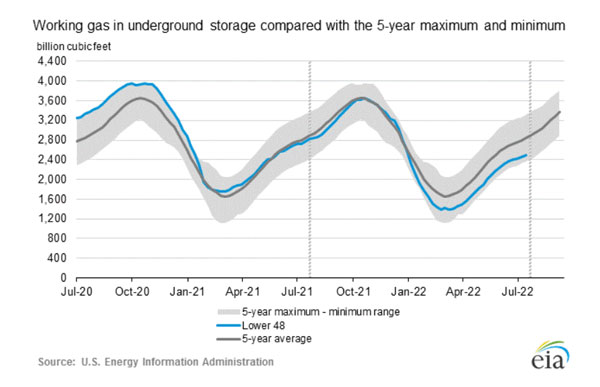

But things could get interesting this winter, given the nearly insatiable global thirst to electrify everything at a time when U.S. natural gas inventories are about two months behind the five-year average.

Connecting the Dots.

LNG is liquefied natural gas, super-chilled to minus 260 degrees.

The U.S. was the world's largest producer and exporter of LNG in the first half 2022, passing both Australia and Qatar. The majority went to Europe and the United Kingdom, where there are a couple dozen LNG terminals.

But then things got complicated.

LNG export capacity expansions in Texas and Louisiana were offset by a fire in June at the Freeport, TX, facility which accounts for about 17 percent of U.S. export capacity.

The Russian Factor.

Natural gas flows on the Nordstream 1 pipeline from Russia to Germany were curtailed a few weeks ago from a 40 percent run rate to 20 percent. And natural gas pipeline exports from Russia to the European Union and United Kingdom are already 50 percent below the five-year average.

In response, the European Union largely agreed to reduce their usage of natural gas by 15 percent from August until March, partly out of concerns that Russia may completely stop the flow of natural gas to Europe.

But reducing natural gas demand may only put more pressure on “readily available” alternate energy sources for electric power generation, such as coal, diesel and LPG.

Many utilities use diesel for their large back-up generators and propane or LPG (propane/butane) to supplement their natural gas supply or to boost line pressure during periods of very strong demand. So there’s a trickle-down effect that impacts multiple fuel sources.

The Australian Factor.

Earlier this month, Australia’s Resources Minister said they’ll decide in October whether or not they need to curb LNG exports in 2023 to avoid a domestic supply shortage due to declining production levels.

Why should we care?

Well, Australia is one of the top 3 LNG exporters in the world. Their largest customers are China and Japan. Those are also Qatar’s largest customers.

What complicates things is that European countries have been requesting more LNG from Qatar since February. If Australia exports less LNG to smaller Asian markets, and Qatar fills in the gaps, where will western Europe get the LNG they need to heat homes, power businesses, and generate electricity.

From the U.S., most likely.

What Does All Of This Mean For Me?

We live in a global community where the price and availability of every substantial source of energy, from LNG to LPG, is inter-connected with events that happen around the world.

Where Propane Prices Could Be Going.

For what it’s worth, Goldman Sachs (a multinational fortune teller) recently revised their Q422 Brent crude price forecast down to the $110.00 to $125.00 range.

This could equal roughly $1.25 to $1.42 per gallon FOB Mt. Belvieu, TX, (50 percent value of WTI and a $5.00/bbl. discount to Brent).

Of course, forecasts aren’t always accurate. A lot can change before and after the mid-term elections.

What Can You Do To Prepare?

The trading community seems to be betting that global supply concerns are less price determining than demand destruction concerns, and will amount to nothing. They may be right.

But why be caught short?

Our advice:

Take a look at your supply and demand forecast for the winter months. If you see any supply gaps, consider targeting those specific months by contracting some winter-only supply with us now, while things are still relatively quiet.

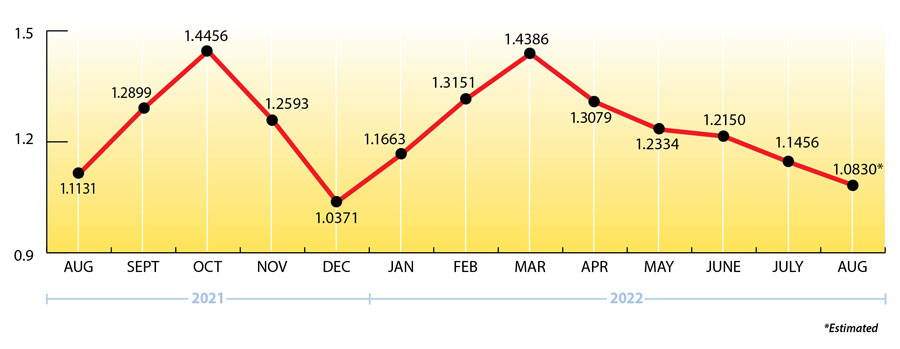

What’s Happening with Propane Prices?

Current prices have been falling since March and are as low as they’ve been since December and, before that, last June.

Will they keep falling? That’s hard to say.

But fundamentals always win out over emotion when necessity kicks in.

Propane Price Chart

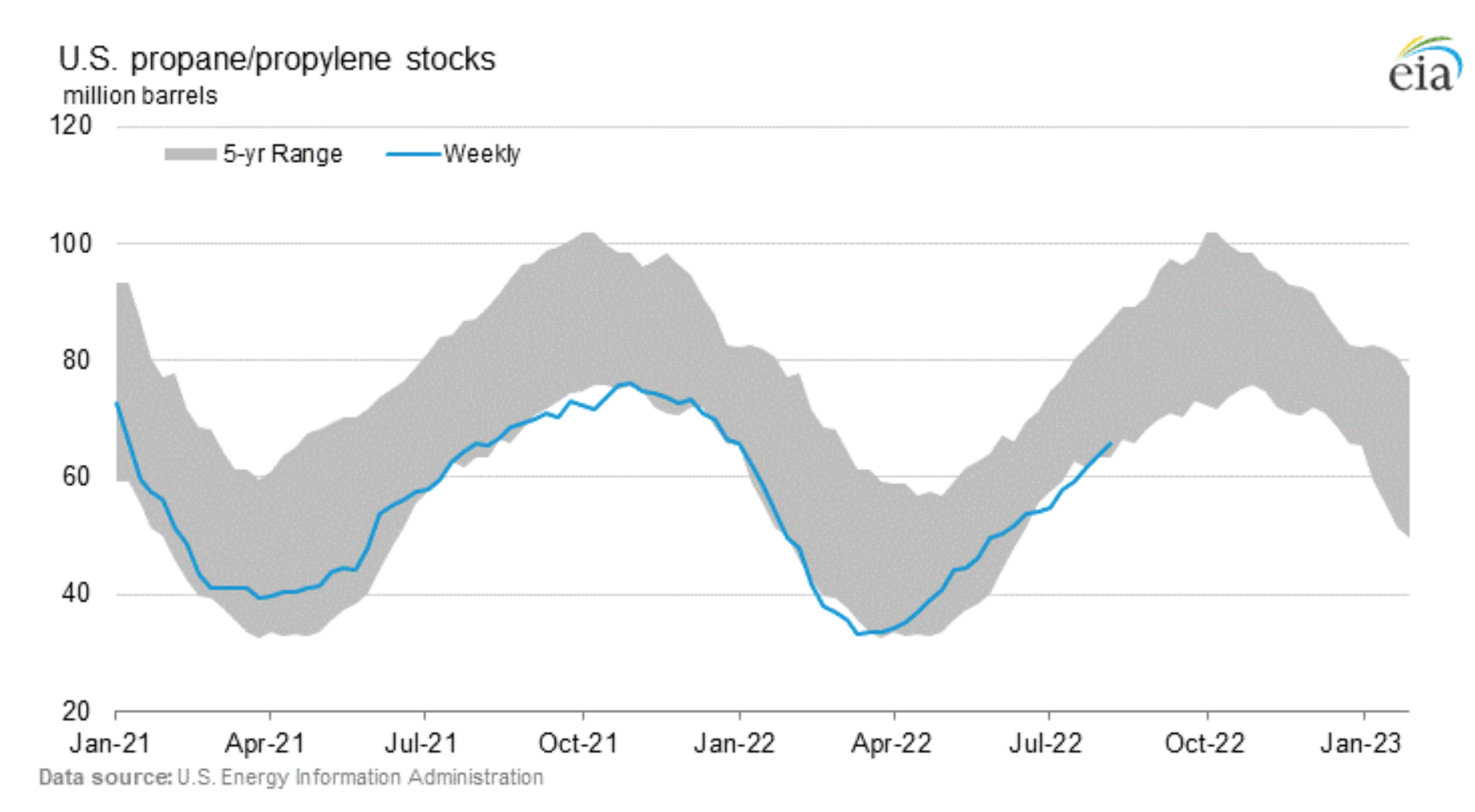

Weekly Inventory Numbers

U.S. propane inventories showed a healthy build of 2.34 mmbbls. for the week ending August 12, 2022, on the higher end of industry expectations.

This brings national inventory levels to 68.00 mmbbls., about 2 percent higher than last year but 8 percent lower than the 5-year average.

PADD 2 (Midwest/Conway) inventories had a modest build of .53 mmbbls. They currently stand at 20.85 mmbbls., largely unchanged from last year.

PADD 3 (Gulf Coast/Belvieu) inventories had a fairly strong build of 1.38 mmbbls. They now stand at 35.86 mmbbls., roughly 6 percent above last year.

The Skinny

A bevy of mostly demand-side reasons, including recessionary concerns, have outweighed a tight physical market for a while now, pushing most energy prices lower.

On a global scale there are still legitimate reasons to be worried about the price and availability of some energy sources for this upcoming winter, especially in Europe.

But nothing happens in a vacuum.

While things are still relatively quiet, please consider reviewing your supply and demand balance for the upcoming winter months and let us know if you need to add any winter-only volume with us.

Get Stephen's insights on propane delivered to your inbox every month.

Sign up for our monthly newsletter here.

For more frequent updates and industry news, join us on LinkedIn.

NOTE: The views and opinions expressed herein are solely those of the author, unless attributed to a third-party source, and do not necessarily reflect the views of Ray Energy Corp, its affiliates, or its employees. The information set forth herein has been obtained or derived from sources believed by the author to be reliable. However, the author does not make any representation or warranty, express or implied, as to the information’s accuracy or completeness, nor does the author recommend that the attached information serve as the basis of any buying decision and it has been provided to you solely for informational purposes. © 2011-2022 Ray Energy Corp. All rights reserved. Any reproduction, representation, adaptation, translation, and/or transformation, in whole or in part by whatsoever process, of this site or of one or several of its components, is forbidden without the express written authorization from Ray Energy Corp.